by ObiTechie's Team | Jul 7, 2023 | FinTech, Money Transfer and Payment

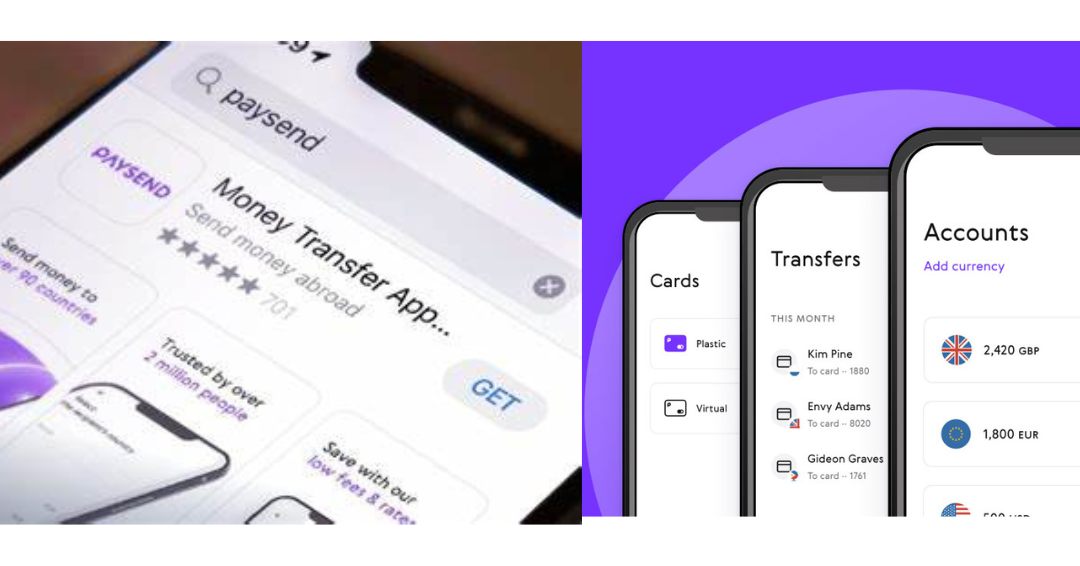

In this era of digital connectivity, money transfers across borders should no longer be a challenge. The process should be as straightforward as sending a text message. Paysend is an innovative global money transfer service, and it is set to make this dream a reality.

What is Paysend?

Paysend was founded in the UK in 2017 and is a pioneering online money transfer platform. A team of experts launched the platform, and it identifies itself as a global Fintech company on a mission to change how money is moved around the world. Paysend has developed a fast, simple money transfer system, acquiring over 4 million customers and 17,000 small and medium-sized businesses globally. The service allows users to conveniently send money from their credit or debit cards directly to their bank accounts, Paysend prepaid cards, or digital wallets. This is in more than 90 countries worldwide.

Since Paysend was founded on the ethos of speed, security, and simplicity, it is committed to making global money transfers effortless. It connects millions of people globally with its easy-to-use service.

Key benefits

Paysend is outstanding among dozens of online money transfer services. These are the main benefits that make it unique.

Simplicity:

Paysend is a straightforward, user-friendly platform that makes sending money online a breeze. All you require are the recipient’s details – name, and bank account number – to initiate a transfer.

Speed:

We are used to traditional wire transfers that take several days to complete a transaction. Paysend processes transfer within minutes. This fast transfer speed is a game-changer for people who need to send money urgently.

Security:

Paysend adheres to strict safety standards when transferring funds. The service is licensed and regulated by the UK’s Financial Conduct Authority (FCA), confirming its commitment to reliability and trustworthiness.

Global Reach:

Paysend facilitates transfers to over 90 countries worldwide. This extensive reach provides an efficient and convenient solution for those with international financial obligations, such as supporting family members overseas or managing business transactions.

Fee

Paysend is also convenient and cost-effective. The platform offers a flat fee structure. You will be charged a constant fee of $2/€2/£2 for each transaction, regardless of the amount you want to transact. There are no additional fees. The rates in this pricing strategy can result in significant savings, particularly when you want to do larger transfers where percentage-based charges could accumulate.

However, please note that even if Paysend does not charge a currency exchange markup, your bank may charge you fees for each transaction or apply a different exchange rate.

How to Send Money Online with Paysend

Transferring money with paysend is quick and easy. The steps are:

1. Create an account: Visit the Paysend website, download the mobile app, and register as a first-time user.

2. Start a transfer: Enter the recipient’s name, bank account details, and the amount you want to send. Paysend will display the flat transfer fee and the exchange rate before you complete the transaction.

3. Make a payment: Pay for your transfer using a debit or credit card. Paysend accepts cards from over 50 countries worldwide.

4. Track your transfer: You can track its progress through your Paysend account once it is underway.

Customer support

Paysend provides strong customer support that ensures uninterrupted customer service. Customer support is available 24/7 through the app or live chat on their website. You can also reach the support team by email. Besides, you can check out their extensive FAQ section on their website to get immediate answers to commonly asked questions.

Article source

Transfer money online globally from Canada for only £1, $2 or €1.5 | Paysend Global Transfers

by ObiTechie's Team | May 30, 2023 | FinTech, PayTech

Throughout centuries, payment systems have undergone a gradual evolution to reach the advanced stage we see today. From the era of barter trade, where goods and services were exchanged for other goods and services, to the introduction of coins and paper money, we have witnessed continual improvements aimed at enhancing efficiency.

In today’s world, we rely on modern technology to process payments through digital methods like mobile wallets and cards. It’s expected that we’ll soon be using digital currencies for payments as well. The need for faster and more secure payment options has led to ongoing advancements in this field. This article gives a comprehensive historical overview of how payment methods have evolved. We focus on the step-by-step from barter trade to the current cryptocurrency systems.

The Dawn of Trade: Bartering Systems

The interesting history of payment systems dates back to the historical barter trade payment methods. The method involved the exchange of goods for goods and services for services. The payment method appears primitive. However, it was necessary, and it helped our forefathers obtain the goods and services they needed to survive. Despite its extraordinary advantage, the barter trade method also had drawbacks because it lacked a standard measure of value. In addition, fulfilling the trade required a coincidence of wants.

The Emergence of Commodity Money: The Introduction of Standardization

Over time, there was a need to overcome the limitations. Therefore, society introduced commodity money, a vital breakthrough in the evolution of payment systems. In the past, people used silver, gold, salt, and livestock as a currency because they were highly sought-after and had inherent value. The transition provided a standard measure of value. In addition, it facilitated trade hence boosting economic activities.

The Birth of Coinage and Paper Money: Formalizing Exchange

The next milestone of payment systems was the introduction of coins. The Lydians produced the first coin around 600 BC. This significant step marked a new beginning of formalized currency. In addition, it allowed the society members to exchange smaller and specific values, increasing trade efficiency.

During the Tang Dynasty, the invention of paper money by the Chinese further revolutionized the payment system. Payments became easier, and paper money was easier to carry around, could represent larger values, and brought forth significant development of complex banking systems to facilitate the production and storage of money—notably, the paper bills required verification and validation systems to establish trust.

Check and Credit Cards: The Shift to Cashless Payments

With time, societies became more complex, with more and more daily transactions. People needed safer and more convenient payment systems. In the 17th century, checks were introduced. Initially, only the wealthy used the checks. Checks allowed people to carry huge sums of money without carrying it in cash.

In the mid-20th century, the Diner’s Club founded the first universal credit card. Credit cards marked a vital shift towards cashless transactions, making payment more straightforward, safer, and convenient. The ability to extend credit made the cards more popular, boosting commerce even more through the digital era.

Electronic Payments and Online Banking: The Dawn of the Digital Age

In the late 20th century, electronic payment systems emerged. ATMs and EFTPOS systems were introduced for automated banking and electronic transactions. The machines made money transfer very convenient. Customers were no longer required to visit banks or carry large amounts of money to make payments.

Further, the PayPal payment system evolved following the rise of the internet. PayPal supported immediate, remote transactions changing the way businesses operated.

Cryptocurrencies and Mobile Payments: The Future of Payment Systems

Currently, we have the most advanced payment systems; mobile payment and cryptocurrency payment methods. Mobile payment apps such as Venmo, Zelle, and Apple Pay have improved the convenience of immediate, peer-to-peer payments directly from users’ smartphones. Also, the sender and recipient can be in a different location.

Cryptocurrencies such as Bitcoin have established a new form of digital asset-based payment. Cryptocurrencies use Blockchain technology, offering a decentralized, secure, and anonymous method of value transfer.

Embracing the Future of Payment Systems

The evolution of payment systems represents humanity’s endless drive to achieve convenience, security, and efficiency. From barter trade to Bitcoin technology, every stage has made payments more effortless, secure, and faster, accelerating global economic growth and connecting people to their desired businesses like never before.

New transaction technologies, such as contactless payments and digital wallets, have emerged as we approach the future. Besides, biometric payment systems are redirecting commerce even more. The continued evolution of payment systems indicates the ingenuity and adaptability of societies, serving as evidence that with trade, innovation is inevitable.

Ultimately, the history of payment systems and their evolution is fascinating. As we advance from one era to the next, we get closer to the seamless, instantaneous, and universally accessible world of transactions. As we anticipate more discoveries in payment systems, the future holds more possibilities in commerce.

Article Sources

https://www.investopedia.com/articles/07/banking.asp

https://www.investopedia.com/ask/answers/061615/what-difference-between-barter-and-currency-systems.asp

https://www.investopedia.com/articles/financialcareers/09/ancient-accounting.asp

https://www.feedough.com/the-evolution-of-payments/

by ObiTechie's Team | Apr 28, 2023 | FinTech

Cryptocurrency is a form of digital or virtual currency. Cryptographic systems secure the coins, and people can use these systems to make safe online transactions without an intermediary. No country or government authorities regulate Cryptocurrencies; therefore, governments don’t intervene in Cryptocurrency transactions. According to Blockchain technology, most of the cryptocurrencies in use are decentralized networks.

FAQ Knowledge base Support team Logout from plugin

People buy Cryptocurrencies from Cryptocurrency exchanges, mine them, or receive them as a reward for completing tasks on the Blockchain. However, not every e-commerce permit purchases using Cryptocurrencies, and you will hardly see any retail business allowing payments using Cryptocurrency, not even the popular ones like Bitcoin. Nonetheless, Cryptocurrency values have made Bitcoins popular as investing and trading instruments. Although some countries may not accept it, people sometimes use Bitcoins for cross-border transfers

The Rise of Cryptocurrency

Cryptocurrency shifted from an academic concept to a virtual reality in 2009 after the creation of Bitcoin. While Bitcoin saw a mass, consistent following in the subsequent years, it also caught the attention of investors and media in April 2013, when it recorded its highest of $266 per Bitcoin after surging ten times in the preceding two months.

Bitcoin recorded a market value of more than $2 billion at its highest. However, it also recorded a 50% plunge shortly after, which sparked a hot debate about the sustainability of Cryptocurrencies in general and Bitcoin specifically.

The Cryptocurrency market has recorded notable positivity because of the simplified microeconomic activities, which have increased the crypto price. Besides, the current trading volume of the Crypto market has risen to the highest mark since June 2021. The daily market volume is approaching $70 billion, while the Crypto market capitalization is $1.20 trillion.

Impact of Cryptocurrency on the Financial Industry

As a part of Cryptocurrency, Bitcoin can potentially dismantle a banking system. The main impacts Cryptocurrency has on the financial industry are:

• Cryptocurrency eliminates double spending. Each Bitcoin is unique, and cryptographically protected. The currency cannot be replicated or hacked. Therefore, you can neither spend the Bitcoin twice nor have it counterfeit. These features are making it more and more attractive in the financial industry.

• Even if the Bitcoin network is decentralized, it is still trustworthy.

• Bitcoin has such a strong network that it makes centralized infrastructure unnecessary. The currency is produced and distributed through a streamlined process.

Challenges and Future of Cryptocurrency

Some economic analysts are already predicting significant changes in the Crypto market as institutional money enters the market. Furthermore, Crypto will likely be floated on the Nasdaq, increasing the Blockchain’s credibility as an alternative to conventional currencies. According to some experts, investing in Bitcoin would be made easier with the availability of a verified exchange-traded fund specifically for cryptocurrencies. However, investors will still be concerned about investing in such digital assets, even if the exchange-trade fund is created, due to the lack of understanding of Crypto; this means the desire will automatically arise.

If you wish to invest in Cryptocurrency, use the same process when considering any other speculative investment. There is always risk of losing some or all your investment, and Cryptocurrency has no permanent benefit apart from what a buyer will pay when a case arises. The currency is susceptible to price swings increasing the chances of loss to an investor.

Some of the challenges Cryptocurrencies are facing:

• A computer crash or hackers ransacking a virtual vault can delete one’s digital fortune. Unfortunately, the current technology has not been able to counter such instances.

• The more popular the Cryptocurrencies become, the more likely they are to face government regulations and scrutiny, which may wear down the fundamental premise of their existence.

• Cryptocurrencies are for the technically adept. Most businesses have embraced Cryptocurrency but still need to work on increasing consumer acceptance.

• Cryptocurrency will likely be highly regulated in the coming years, which may give way to alternative currencies. Cryptocurrency must be mathematically complex to prevent hackers from accessing the systems, yet easy for consumers to understand. Crypto needs to be decentralized but with adequate protection and anonymity without being a means to evade tax, money laundering, and other notorious activities.

Conclusion

The rise of Bitcoin has led to a debate concerning its future with other Cryptocurrencies. Although Bitcoin has faced diverse issues, its success since its launch in 2009 has led to the creation of alternative Cryptocurrencies such as Ripple, Ethereum, and Litecoin. Therefore, Cryptocurrency will need to satisfy wildly divergent criteria and overcome its challenges to attract more investors and maintain credibility with the current users.

Article Source:

What the future holds for cryptocurrencies | World Economic Forum (weforum.org)

The Rise of Cryptocurrency and its Impact on the Financial Industry (fidomoney.com)

Where Is the Cryptocurrency Industry Headed in 2021? (investopedia.com)

by ObiTechie's Team | Apr 26, 2023 | FinTech

Photo: Forbes and Canva

The FinTech industry is popularly known for its unending innovations. The sector operates within complex systems, including start-ups, financial service providers, and banks. In the recent past, FinTech has relied heavily on machine learning and artificial intelligence for strategic customer insights, improving digital transactions experience, decision-making, and understanding customer purchasing behaviour. This article will explore the role of AI in Fintech, its benefits, and its limitations.

What is Fintech?

As defined by Investopedia, fintech refers to the use of new technology to enhance and automate the delivery and utilization of financial services. The primary purpose of fintech is to assist business owners, organizations, and consumers in better managing their financial operations, lives, and processes. The technology consists of specialized algorithms and software applications that can run on computers and smartphones.

Fintech emerged in the 21st century. When the technology was new, it was only applicable to the backend systems of the foundation of financial institutions like banks. However, from 2018 to 2022, the practice shifted to customer-oriented services, and fintech started including other industries such as retail banking, investment management, education, fundraising, non-profits, and many others.

Currently, fintech is the leading payment and data solution software in the high-end alcohol and beverage industry. Fintech’s primarily aims to empower suppliers, retailers, and distributors by streaming data insights and automating invoice payments. In addition, fintech has been in the market for over 30 years, confirming its dependability and reliable experience.

What is Artificial Intelligence?

Artificial intelligence (AI) is software that operates like human beings, and the software imitates learning patterns and human behaviours using digital programs. In the recent past, companies were reluctant to embrace AI. However, businesses are increasingly turning to AI solutions to enhance the efficiency and productivity of their operations and automate manual tasks.

Artificial intelligence can also be used, for simple to complex tasks in diverse business departments, from data analysis to sales, customer service, and IT tasks automation.

AI in Fintech

There are several benefits businesses can leap from using fintech technology driven by AI. The primary benefits are:

Personalized Financial Services

The primary solution AI provides to fintech companies is the ability to use customer data effectively. With AI, companies can identify customers’ preferences and tailor financial services to meet specific needs. A good example is how Banks can use AI-powered credit systems to analyse a customer’s income and expense history before providing loan assistance.

Efficiency and Cost Reduction

Before the incorporation of AI into fintech, financial services, and products were a realm of branches, and desktops and representatives were present in the workspace. Conversely, artificial intelligence automation in fintech has improved companies’ efficiency and reduced the cost of processing financial transactions for customers.

Risk Management and Fraud Prevention

With AI integrated into fintech, the system can prevent fraud by flagging information about unauthorized payments. The system can detect any transaction anomaly through data analytics stored in the system.

Challenges and Limitations

According to the US Department of the Treasury, whiles fintech firms provide valuable services to businesses, there is a need to be cautious due to data privacy and regulatory arbitrage, which is a big concern.

The technology has weak regulation. In the world of cryptocurrencies, the forms of fundraising are unregulated and have become firm grounds for fraud and scams.

Most of all, access to data is critical for AI to be more effective in its deliveries. Therefore, fintech companies must constantly address any form of limitation of extensive data to train AI algorithms.

In Summary

Artificial intelligence in fintech is here to stay. The technology is used for various purposes in the financial sector, and its solutions are customer support, credit risk assessment, lending decision-making, wealth management, fraud detection, and many more. Currently, fintech companies are using artificial intelligence for improvised precision levels, enhanced efficiencies, and high-speed query resolution.

AI in fintech accelerates innovation leading to fast, personalized, and secure services with high-level customer satisfaction and global reach.

Article Sources

Financial Technology (Fintech): Its Uses and Impact on Our Lives. https://www.investopedia.com/terms/f/fintech.asp

Wealthy Asians dash to ditch their US passports. (2015, February 1). AsianInvestor, 35.